New local partnership agreements are needed between purchasing authorities and independent providers.

- Many local authorities find capacity in local independent provision to be unavailable, often due to places being in use by other local authorities from further afield.

- Frameworks and Dynamic Purchasing Systems do not offer incentive to local providers to grant preferred access to the local authorities where the provider services are located.

- There is commercial imbalance in parts of the children’s services sector that can result in prices and profit levels becoming inconsistent with a market “functioning effectively”. (CMA final report – March 2022).

- Use of block contracts and soft block contracts remains at relatively low levels compared to the various forms of spot purchasing (both within and outside of formally procured arrangements).

Commercial and financial arrangements are too prominent and influential in this sector. They need to be moved out of the way of professional decision making around the needs of children and young people.

A new form of commercial model to bring purchasers and providers closer together.

Key elements of the model:

- De-risking the fixed cost base of provider services through annual contributions from the host authority or region.

- Preferred access to local services for local councils or regions.

- Purchaser option to release capacity for other local authority use. Shared incentives with provider.

- Compensation to the host authority if placements are made into the provider’s local service from an outside authority.

- Overall profit/surplus-sharing mechanism between local purchaser(s) and local service provider(s) with escalating benefit to local authority for maximum use of the local provision.

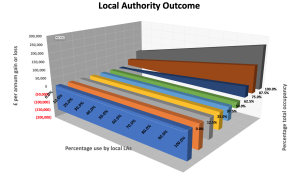

The model has been built to allow purchasers and providers to try different permutations and to illustrate the results for their organisation at all possible levels of occupancy and use by the local council or region.

The model has been built to allow purchasers and providers to try different permutations and to illustrate the results for their organisation at all possible levels of occupancy and use by the local council or region.

This allows parties to visualise the rewards and risks of the arrangements across all possible outcomes, and to alter parameter values to experiment with different levels of contributions and profit shares.

Facilitated use of the tool would allow local authorities or regions and their local providers to find out if there are values of contributions and profit sharing that would be acceptable to all parties. If there are such values these would form the commercial basis of new local partnerships that moves commercial arrangements out of the way of professional decision making.

Benefits

- Closer partnerships at a local level between purchasers and providers to benefit children and young people

- Removes the influence of commercial and financial factors from professional decision making around the child

- Transparency and clarity of economic risk sharing

- A flexible, adaptable model that can be developed through use and experience

- Rebalanced markets with longer term sustainability

Are you interested?

We are in the process of introducing this model to the first region in England and would welcome contact from you if you are from a local authority, a regional commissioning team, a regional care cooperative or a provider organisation who would like to know more.

We will be running workshops to illustrate this model on 5th March and 14th March 2024 at 10:30am. The first 20 places are free to attend.

If you would like to secure a place please provide your contact details via contact@revolution-consulting.org